Fixed cost shown in graph:

Variable cost shown in graph.

Semi-variable cost shown in graph.

Fixed Budgets:

A fixed budget sets spending amounts that don't change, no matter what happens. A fixed budget is a budget that does not change or flex when production, sales or some other activity increases or decreases. A fixed budget is also referred to as a static budget.

Example: A company plans to spend Tk. 50,000 on marketing every month, regardless of whether sales go up or down. Fixed Budgets like as:

| Name of cost | Present sales | Increase Sales | Decrease Sales |

| Marketing expenses | Tk.50,000 | Tk.50,000 | Tk.50,000 |

Flexible Budgets:

Flexible budgets are budget plans that adjust according to changes in activity levels or sales volumes. It can change or flex when production, sales or some other activity increases or decreases. A flexible budget is also referred to as a variable budget.

Example: A company decides to spend Tk. 10 for every unit sold on marketing.

Flexible Budgets like as:

| Name of cost | Present sales 5000 units | Increase Sales 8,000 units | Decrease Sales 4,000 units |

| Marketing expenses Per unit Tk.10 | Tk.50,000 | Tk.80,000 | Tk.40,000 |

At last we say that, fixed budget is same on all activity level but flexible budget is variable.

Basically, flexible budgets provided more advantage to business and non-business organization. Some important discuss here,

1. Decision-Making:

business can make better and perfect decision with actual revenue and cost prediction using flexible budgets.

2. Cost Control:

Perfect cost estimation can be possible using flexible budgets and it can help to reduce cost of the organization.

3. Risk Management:

It can help to reduce risk by providing a clean picture of future revenue at different activity level.

4. Improve Plan:

flexible budget helps to make proper production or sales plan which level of activity gives higher profit.

5. Performance Evaluation:

It can help to evaluate at which level of activity gives better performance or gives higher profit by using lower cost.

At last we say that, flexible budgets help to make more effective and realistic decision.

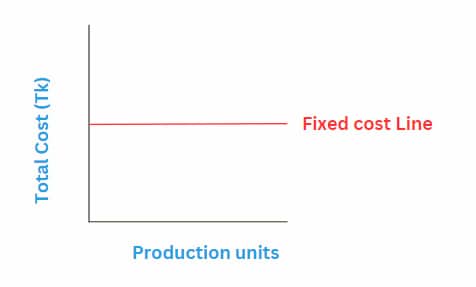

Fixed cost (স্থায়ী ব্যয়): Fixed costs are those that stay the same in total regardless of the number of units produced or sold. Although total fixed costs are the same, fixed cost per unit changes as fewer or more units are produced.

Example: A company plans to spend Tk. 50,000 on marketing every month, regardless of whether sales go up or down. Fixed Budgets like as:

| Name of cost | Present sales 5,000 units | Increase Sales 8,000 units | Decrease Sales 4,000 units |

| Marketing expenses (total cost) | Tk.50,000 | Tk.50,000 | Tk.50,000 |

| Marketing Expenses (per unit) | Tk.10 | Tk.6.25 | Tk.12.5 |

Fixed cost shown in graph.

At last we say that, fixed cost total fixed but per unit variable.

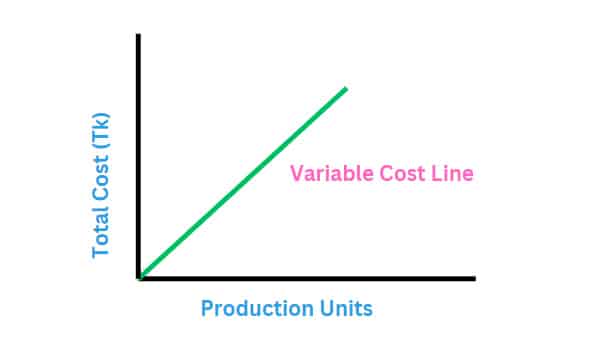

Variable cost (পরিবর্তনশীল ব্যয়): Variable costs are the costs that change in total each time an additional units produced or sold. With a variable cost, the per unit cost stays the same, but the more unit produced or sold higher the total cost.

Example: A company decides to spend Tk. 10 for every unit sold on marketing.

Flexible Budgets like as:

| Name of cost | Present sales 5000 units | Increase Sales 8,000 units | Decrease Sales 4,000 units |

| Marketing expenses (Total cost) | Tk.50,000 | Tk.80,000 | Tk.40,000 |

| Per Unit Cost | Tk.10 | Tk.10 | Tk.10 |

Variable cost shown in graph.

At last we say that, Variable cost total variable but per units Fixed.

The statement “Fixed cost per unit is variable but variable cost per unit remains fixed” may appear paradoxical at first, but it highlights an important concept in cost analysis. Discuss details in bellow: -

Fixed cost (স্থায়ী ব্যয়): Fixed costs are those that stay the same in total regardless of the number of units produced or sold. Although total fixed costs are the same, fixed cost per unit changes as fewer or more units are produced.

Example: A company plans to spend Tk. 50,000 on marketing every month, regardless of whether sales go up or down. Fixed Budgets like as:

| Name of cost | Present sales 5,000 units | Increase Sales 8,000 units | Decrease Sales 4,000 units |

| Marketing expenses (total cost) | Tk.50,000 | Tk.50,000 | Tk.50,000 |

| Marketing Expenses (per unit) | Tk.10 | Tk.6.25 | Tk.12.5 |

Variable cost (পরিবর্তনশীল ব্যয়): Variable costs are the costs that change in total each time an additional units produced or sold. With a variable cost, the per unit cost stays the same, but the more unit produced or sold higher the total cost.

Example: A company decides to spend Tk. 10 for every unit sold on marketing.

Flexible Budgets like as:

| Name of cost | Present sales 5000 units | Increase Sales 8,000 units | Decrease Sales 4,000 units |

| Marketing expenses (Total cost) | Tk.50,000 | Tk.80,000 | Tk.40,000 |

| Marketing expenses (Per Unit Cost) | Tk.10 | Tk.10 | Tk.10 |

At last we Proved in table “Fixed cost per unit is variable but variable cost per unit remains fixed”.

| Key difference | Fixed Budget( স্থায়ী বাজেট) | Flexible Budget(নমনীয় বাজেট) |

| Meaning | The budget designed to remain constant, regardless of the activity level reached is fixed budget. | The budget designed to change with the change in the activity level is flexible budget. |

| Nature | static | Dynamic |

| Activity level | Only one | Multiple |

| Estimates | Base on assumption | Realistic and practical |

| Examples | Depreciation ,rent, salary, insurance, tax etc. | Material, labor, commission on sale, packing exp etc. |

| Per unit | Per unit cost variable | Per unit cost fixed |

Cost segregation is very important for business to better understand their cost structure and make proper financial decision. Cost segregation is a process that basically use hi-low method to identify the fixed and variable elements of the semi-variable costs.

Example: Let, total Production Cost Tk.3,00,000 for 4000 units and total Production Cost Tk.3,90,000 for 7000 units

Step: 01

Calculate Variable cost = Change in Tk ÷ Change in Unit = 90,000 ÷ 3,000 = 30

Step: 02

Calculate Fixed cost = Amount — (Unit × Rate )

= 3,00,000 — (4,000 × 30)

= 1,80,000

At last we say that, it can help to estimate cost structure and actual cost for business.